Committees At Work

PWB Hard Hats & Hot Shots: EPAB Trap Shoot

The EPAB Trap Shoot is entering an exciting new chapter as a fundraiser benefiting the Professional Women in Building (PWB) Council. While the purpose has evolved, everything participants love about the event remains the same—the friendly competition, great networking, and unforgettable day on the range. Teams will still battle for bragging rights, awards, and the coveted top spots, bringing the same energy and competitive spirit year after year. Every shot taken will now help support PWB programs, scholarships, leadership development, and community outreach initiatives. By participating, you're not only enjoying one of EPAB's favorite traditions, but also investing in the growth and success of future leaders in our industry. Join us as we continue this exciting tradition with a renewed purpose and an even greater impact. Register your team or find sponsorship opportunities at www.elpasobuilders.com.

General Meeting – Sept. 10, 2026, Airport Radisson

Join us for our upcoming EPAB General Membership Meeting! Connect with fellow industry professionals, enjoy valuable networking opportunities, and stay informed on the latest association and industry updates. Our featured speaker will be announced soon, and you won't want to miss what's in store. Reserve your seat today and be part of the conversation!

Gofl Tournament & Clubhouse Social

Teams have sold out but if you would still like to be a part of the day’s events, contact Committee chair Raul at (915) 497-6118 or Ceci (915) 778-5387 for more information or visit the event webpage at www.elpasobuilders.com.

Parade of Homes- Coming October 9, 2026!

Scheduled to start in October look out for tickets to go on sale soon! Featured builders will be Crown Heritage Homes, Cullers Homes, Hakes Brothers, ICON Homes, MA Homes, Pacifica Homes, Pointe Homes, and Winton Homes. Look for sponsorship opportunities and special events coming soon!

Workforce Development – John Chaney

Efforts are underway to speak with local school district officials, builders and small businesses to stress the importance of promoting careers in the trades. Committee has begun compiling pertinent information and are working on a webpage where all relevant information can be found. Look for that to launch before the end of August.

SAVE THE DATE – November 5, 2026

HomePAC Fundraiser “Harvesting Success” (BBQ Plate sale) – Edgar Garcia

Fire up your appetite and support industry advocacy! Join us for the HomePAC BBQ Plate Fundraiser, where our talented builder members will be smoking delicious brisket and sausage plates for purchase by EPAB members and their office teams. Every plate sold ($25 each) helps strengthen HomePAC, supporting the advocacy efforts that protect and advance the residential building industry in Texas. Enjoy a great meal while making a meaningful investment in the future of our industry—because every bite builds a stronger voice!

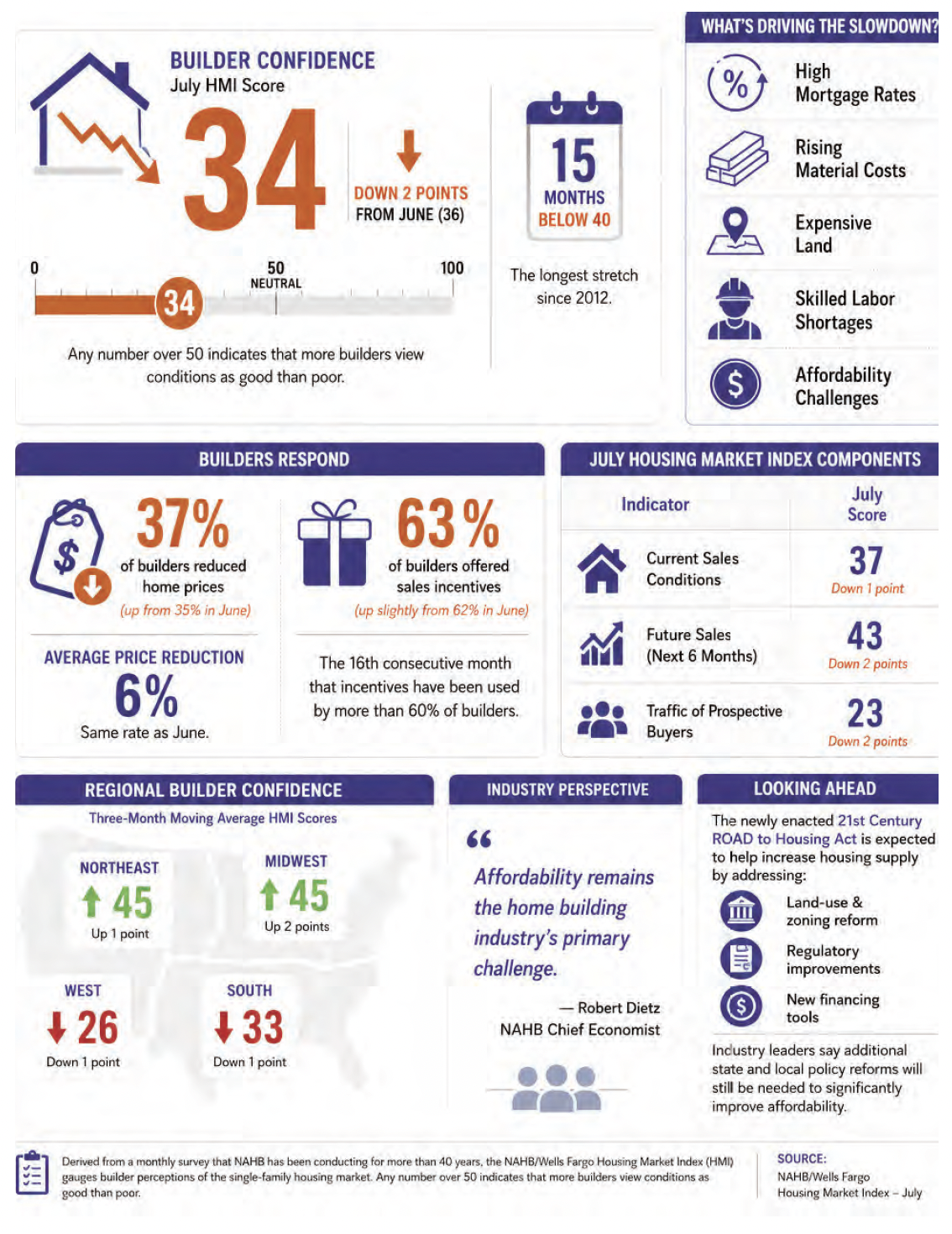

New Home Sales Edge Higher

Affordability challenges continued to weigh on the new-home market in June, as elevated mortgage rates, rising inflation and broader economic uncertainty kept many prospective buyers on the sidelines.

Sales of newly built single-family home rose 1.6% in June to a seasonally adjusted annual rate of 628,000, up from an upwardly revised May estimate, according to newly released data from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau. The pace of new home sales is down 5.6% from a year earlier.

“The pace of new home sales has remained constrained in recent months by elevated mortgage rates,” said Bill Owens, chairman of the National Association of Home Builders (NAHB) and a home builder and remodeler from Worthington, Ohio. “Builders continue to use incentives to support sales, with NAHB survey data showing that 62% of builders offered some form of incentive in June.”

“New home sales are gaining some momentum at the more affordable range of the market, with homes priced below $300,000 accounting for 23% of June sales, up from 16% a year earlier,” said NAHB Chief Economist Robert Dietz. “However, that price point is generally only achievable in markets with lower development and construction costs, particularly with respect to lower state and local regulatory costs.”

A new home sale occurs when a sales contract is signed, or a deposit is accepted. The home can be in any stage of construction: not yet started, under construction or completed. In addition to adjusting for seasonal effects, the June reading of 628,000 units is the number of homes that would sell if this pace continued for the next 12 months.

New single-family home inventory in June was virtually unchanged at 485,000 units, down 0.2% from May, and down 3.2% compared to a year ago. This represents an elevated 9.3 months’ supply at the current building pace. According to NAHB analysis, due to rising resale single-family inventory and elevated new construction inventory, combined new and existing home inventory stands at just above a 5.2 months supply, the highest level since the fall of 2014.

The median new home sale price in June fell 3.3% from May to $398,300, and was down 2.7% from a year ago, largely due to builder price cuts and some geographic shift in mix to the more affordable Midwest.

Regionally, on a year-to-date basis, new home sales are up 2.6% in the Midwest but fell in the other three regions, with declines of 4.7% in Northeast, 4.9% in the South and 10.1% in the West.

ECONOMIC OUTLOOK

Elliot Eisenberg, Ph.D. is an internationally acclaimed economist and public speaker specializing in making economics fun, relevant and educational. Dr. Eisenberg earned a B.A. in economics with first class honors from McGill University in Montreal, as well as a Master and Ph.D. in public administration from Syracuse University. Eisenberg is the Chief Economist for GraphsandLaughs, LLC, a Miami-based economic consultancy that serves a variety of clients across the United States. He writes a syndicated column and authors a daily 70-word commentary on the economy that is available at www.econ70.com.

SPREAD SWING

When financing conditions are easy and investors expect rate cuts, as was the case early this year, the search for extra income/yield by investors intensifies. Capital moves from Treasuries into investment-grade, from investment-grade to high-yield, and from stronger speculative-grade to weaker. So expected rate cuts not only reduce rates, but also rate spreads between bond types, which lowers rates still further. Since the US-Iran War this process has meaningfully reversed.

MIRACLE MILE

The Friday File: Last week, Josh Kerr ran a 3:42.66 mile breaking the previous mark of 3:43.13 seconds, set in 1999, by a gargantuan almost half second! During this historic race Kerr ran at an average speed of 15.51 MPH. He wore bespoke spikes with a carbon plate and aggressive rocker for propulsion, titanium pins to minimize weight and a bespoke speed suit that improved his aerodynamics.

MIDYEAR MOMENTUM

Since 1950, 17 times including this year, the S&P 500 has been up 5%-10% at midyear. The average return during the second half of the year has been 6.6% (better than the post-1949 average of 4.9%) and the median has been 5.7% (slightly below the post-1949 median of 6.3%). Moreover, only in 2007 and 2011 (12.5% of the time) were returns negative in the second half of the year.

CLAIMS CONUNDRUM

Job growth over the past year has been very weak, yet initial jobless claims have been surprisingly low for some time. While this may indicate a labor market that’s fine, I’m suspicious. I suspect layoffs are not occurring in manufacturing, where you go straight to the unemployment office once laid off, but rather in services. There, laid-off workers often receive severance packages that delay/reduce their eligibility for unemployment benefits.

MULTIFAMILY MIASMA

June housing starts blew the proverbial roof off. Headline starts surged 19% M-o-M to 1.427 million annualized units. Regrettably, single-family starts slid 0.2%, continuing their slow, steady 2.5-year deterioration, while the lumpy, noisy, and volatile multifamily sector saw starts soar 76.2% M-o-M to a three year high of 532k annualized units. This will add to the rental supply overhang, which will reinforce the downtrend in the shelter components in CPI.

BOOMER BONANZA

Boomers, those currently between 62-80 years-old, perhaps surprisingly comprise the largest share of US home buyers at 42%. In part, it’s because they (and those over 80) control $110 trillion or about 60% of all U.S. household wealth. With that money they are increasingly upsizing their homes by buying bigger ones or financing additions to existing homes. In 2016 4% upsized, it’s now 7%.

PROFESSORIAL PROOF

The Friday File: For almost 20 years, the average in Brown University’s Welfare Economics and Social Choice Theory in-class midterm was 65-80. This year it was take-home; the average was 96. Suspecting AI cheating, the same professor who taught the course since inception made the final in-class. 18 students dropped, nine didn’t take the final, and the average fell to 48.6 from, at worst, a 65. QED (quod erat demonstrandum).

RESILIENCE REINFORCED

June M-o-M retail sales rose solidly at 0.2% with May revised upwards, weekly first-time unemployment claims remain very low at 208,000, the July Philadelphia Fed Manufacturing Index soared to 41.4, and the Empire State Manufacturing Index jumped to 15.6. Add inflation that in May/June was listless, a Beige Book that’s decent, and Small Business Optimism that rose. All this points to continued economic resilience and no rate hike anytime soon.